Key Takeaway

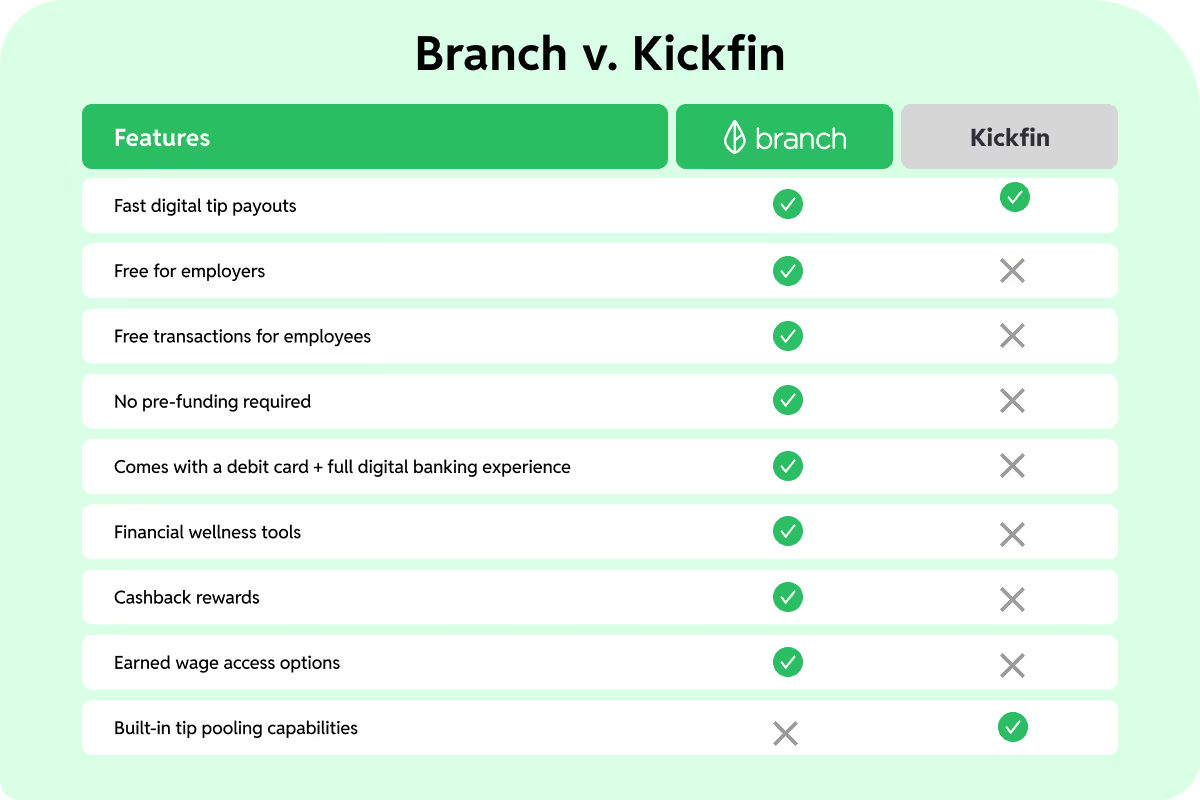

Branch offers superior value for cashless tip distribution with fee-free banking options and comprehensive financial services. Kickfin charges $75-$100 monthly per location. In our analysis, we found Branch provides more payment flexibility and better support for unbanked workers.

Quick Navigation

- Platform Comparison Overview

- Where Payouts Are Sent

- Fee Structure Comparison

- Additional Payment Features

- Tip Pooling Methods

- Financial Wellness Tools

- Frequently Asked Questions

Key Terms

You're done with the hassles of paying out tips in cash: constantly making trips to the bank, reconciling the till, or even putting tips on employee paychecks—which we know isn't fast enough for most workers. But even if your business is ready for cashless tip payouts, how do you know which tip distribution solution is right for your business?

Both Branch and Kickfin offer ways to streamline the tip payout process for service-based businesses, helping you ditch slow, outdated processes like cash and paper checks by switching to fast, cashless tips instead. However, there are a few key differences between the two solutions.

What Are the Key Differences Between Branch and Kickfin?

Where Can Tip Payouts Be Sent?

The destination of tip payouts significantly impacts which employees can benefit from your chosen cashless tipping solution.

Branch Payout Options

With Branch, there are multiple ways you can send tip payouts:

- Branch App & Card — Banking with fee-free options

- Branch Direct — Payouts to existing bank accounts

Advantages:

- Supports unbanked workers

- Accommodates minors 14+

- Provides first-time banking opportunities

- Helps build banking history for loans/mortgages

Kickfin Payout Options

With Kickfin's tip management platform, there is only one place tips can be sent: to your employees' existing bank accounts.

Limitations:

- Excludes unbanked workers

- No support for minors without bank accounts

- Limited flexibility for workers

At Branch, we feel that this flexibility helps you support more of your workforce. For example, unbanked workers, workers with limited documentation, and minors 14+ who may not have an existing bank account can use their free Branch account as a full digital banking experience.

How Do the Fee Structures Compare?

A cashless tipping solution can streamline the payout process and improve your workers' day-to-day lives. However, a cashless tipping solution that benefits both your business and your team should be cost-effective—not filled with fees.

Branch Fee Structure

What's Free:

- No monthly fees for employers

- Free transaction options available

- Banking with fee-free options for workers

Kickfin Fee Structure

Required Fees:

- $75-$100 monthly per location

- Per-transaction fees

- Fees can be passed to employees

💡 Branch saves businesses $900-$1,200 annually per location compared to Kickfin's monthly fees

Offering a new financial solution to your workforce is great, but if it comes with hidden fees, it may do more harm than good.

What Additional Payment Options Are Available?

Kickfin is a tip management platform, so tip payouts are their only focus. Branch is a workforce payments platform with multiple capabilities, including tip payouts.

Branch Capabilities

- Cashless tip payouts

- Direct deposit for regular wages

- Off-cycle payments and bonuses

- Earned wage access (EWA)

- Financial wellness tools

Kickfin Capabilities

- Tip distribution only

- Basic tip pooling

Earned wage access (EWA) is a feature that allows employees to request an advance of a portion of their wages before payday. It can be used to cover emergency expenses or other unexpected needs. This gives your other employees—like managers and back-of-house staff—access to their earned wages daily, so everyone on your staff has an option to access their earnings more quickly.

Is Pre-Funding Required?

While looking for a tip payouts solution, you may see that many providers require pre-funding. Pre-funding means that your company will need to put money in a separate account to fund employee payouts.

Branch Pre-Funding

Not Required:

- We front the money to workers

- Full capital availability

- Simplified cash flow management

Kickfin Pre-Funding

Required:

- Must maintain pre-funded account

- Ties up business capital

- Additional cash flow management

What Financial Wellness Features Are Included?

At Branch, our mission has always been to improve the lives of workers. That's why our service includes financial wellness tools to help your workers budget, save, and find new financial opportunities.

Branch Financial Features

- Cashback rewards on purchases

- Personalized spending insights

- Savings goal features

- Greenhouse marketplace for financial products

- Access to loans and refinancing options

Kickfin Financial Features

- Basic tip payout functionality

- No additional financial services

📊 91% of employees say they would feel more invested in staying at their company if it offered financial benefits that met their specific needs.

How Do Tip Pooling Methods Differ?

Tip pooling has become an increasingly important way for service-based businesses to streamline the payout process. With tip pooling, all of the earned tips are combined, then divided among employees either evenly or based on an agreed-upon ratio.

Branch Tip Pooling

- Partnership with Gratuity Solutions

- Complex tip pooling rules supported

- Automated seamless payouts

- Streamlined start-to-finish process

Kickfin Tip Pooling

- Built-in tip pooling functionality

- Basic distribution rules

For more detailed information about tip pooling strategies, check out our comprehensive blog post.

Frequently Asked Questions About Cashless Tipping Solutions

What is the main difference between Branch and Kickfin?

Branch offers both bank account and direct deposit options for workers. Kickfin only supports existing bank accounts and charges $75-$100 monthly per location.

Which cashless tipping solution has lower fees?

Branch is free for employers. Kickfin charges $75-$100 per month per location plus transaction fees.

Do both platforms support tip pooling?

Yes, both support tip pooling. Kickfin has built-in functionality, while Branch partners with Gratuity Solutions for complex tip pooling rules.

Which platform is better for unbanked employees?

Branch is better for unbanked workers because it provides free bank accounts and debit cards for employees who don't have existing banking relationships.

How to Choose the Best Tip Distribution Solution for Your Business

Both Branch and Kickfin make it simple to switch to cashless tip payouts. This can improve the lives of your employees and make day-to-day operations easier for you. Yet the two solutions have some notable differences, namely: fee structure, where the tip payouts are sent, and what additional financial services or features the solution comes with.

When choosing between Branch or Kickfin for your tip payouts, it pays to weigh your options and find the solution that's the best fit for you. In our experience working with service-based businesses, we've found that comprehensive solutions with fee-free banking options provide the best long-term value for both employers and employees.

Continue reading

.png)

Unlock a Happier, More Productive Workforce